Indian Point nuclear power plant, on the east shore of the Hudson River, in northwest Westchester County, north of New York City. Units 2 and 3, shown in photo, were permanently shut at midnight on April 30, 2020 and April 30, 2021, respectively. A smaller, prototype reactor, Unit 1, operated from 1962 to 1974. Photo: Eric Harvey for the Peekskill Herald, published Sept 24, 2024.

Once upon a time, hearing “disaster” and “Indian Point” in the same sentence probably meant that the nuke plant had just spilled radiation into the Hudson. Or maybe a whistle-blower was postulating a meltdown scenario that could trigger a lengthy shutdown, ensuring the plant’s capacity average wouldn’t surpass 50% — the generating equivalent of a ballplayer batting .200.

But that was last-century. Now nukes are climate-friendly, thanks to atomic fission’s sidestepping fossil fuels’ heat-trapping carbon emissions. Not only that, at century’s end Indian Point vanquished its on-line reliability problems. Starting in 2001, it racked up year after year of chart-topping generating performance right up to the plant’s forced demise that commenced five years ago tonight.

From a climate standpoint, the true Indian Point disaster is the plant’s closure and dismantlement. Both reactors are now kaput, their reactor cores chopped up. Unsurprisingly, the effort to decarbonize the state power grid — New York’s lowest-hanging climate fruit — is in reverse. Emissions are mounting, and in New York City and other downstate areas formerly supplied by Indian Point, electricity is getting costlier and less dependable.

From a climate standpoint, the true Indian Point disaster is the plant’s closure and dismantlement. Both reactors are now kaput, their reactor cores chopped up. Unsurprisingly, the effort to decarbonize the state power grid — New York’s lowest-hanging climate fruit — is in reverse. Emissions are mounting, and in New York City and other downstate areas formerly supplied by Indian Point, electricity is getting costlier and less dependable.

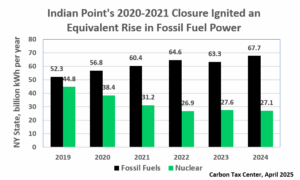

Turning off Indian Point has devastated electricity decarbonization in NY State

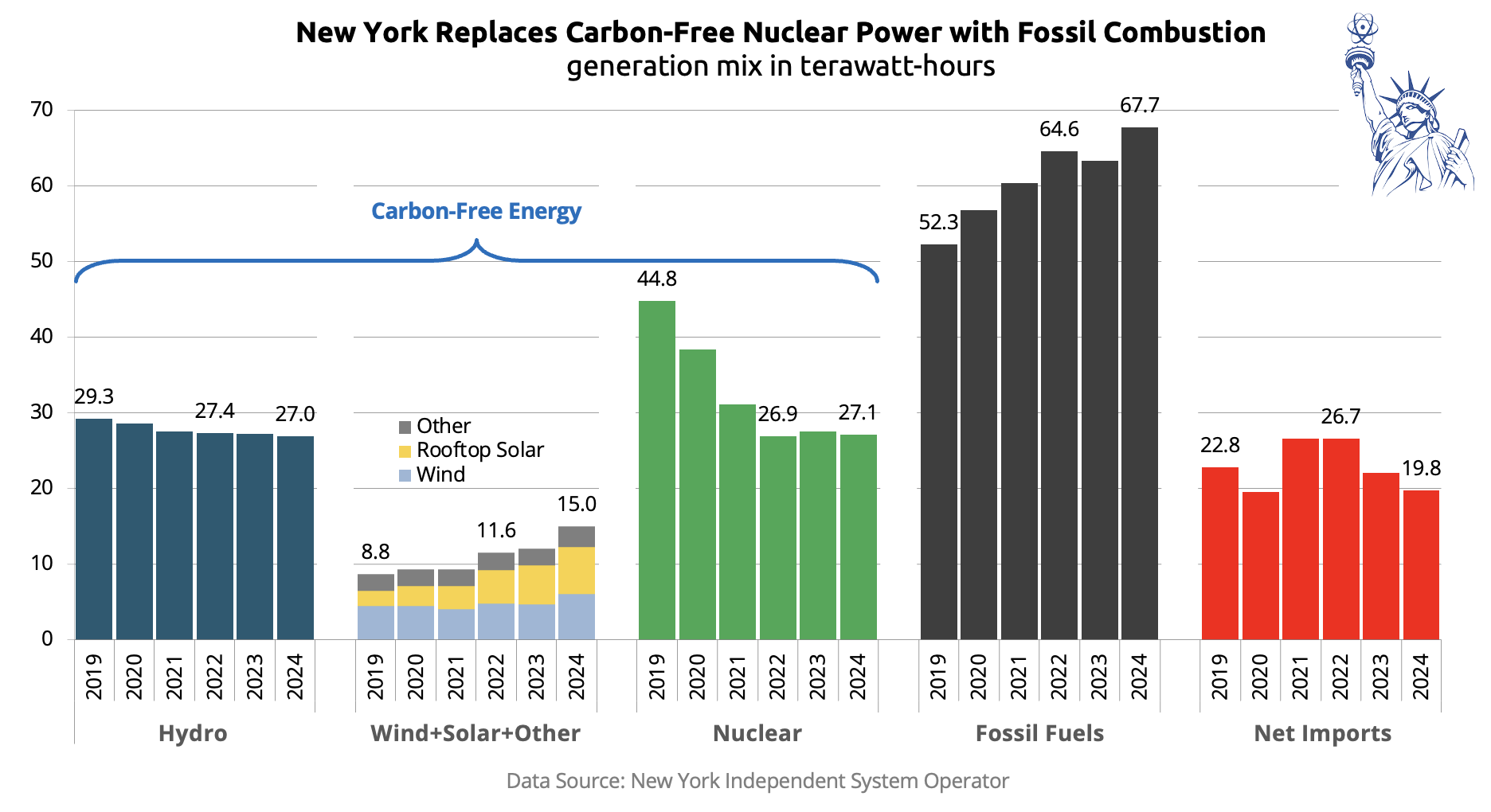

Rarely are opposing trends as clear as the two in the chart directly below. In the five years from 2019, just before Indian Point’s closure began, the amount of electricity made by burning fossil fuels in New York State grew in tandem with the drop in nuclear generation caused by Indian Point’s absence.

Over that 5-year term, as electricity generated statewide with nuclear power fell by 17.7 TWh, electricity generated with fossil fuels (essentially fracked methane gas) rose by 15.4 TWh a year. (A TWh, or terawatt-hour (TWh), equals a billion kWh’s.)

Chart by writer, from NYISO data extracted by Isuru Seneviratne. More details in paragraph directly below.

The loss of generation from Indian Point — 16 to 17 TWh a year, based on the 2001-2019 average — was supposed to be made up with “renewables.” Shutdown proponents, led by the advocacy group Riverkeeper, practically guaranteed it. A press release that the group issued as the hours counted down on April 30, 2020 was titled Indian Point 2 shuts down; NY’s renewable energy transition, for example. (Connoisseurs of the legendary “Dewey Defeats Truman” headline should flock to that Riverkeeper web page.) Yet increases in renewables can barely be detected in 2019-2024 statewide generation changes.

Over those five years, electricity produced statewide from wind, solar and burning forest products did grow by a healthy 70 percent. But because the starting base was small, the increase in absolute terms was a modest 6.2 TWh. Hydro-electricity, moreover, fell by 2.3 TWh, cutting the net 2019-2024 boost from renewables to a measly 3.9 terawatt-hours. Virtually the entire slack from shutting Indian Point had to be taken up by increased burning of fossil fuels — not because of gas greedheads but because no other power source was available. (The various 2019-2024 generation changes meticulously compiled by the NY Independent System Operator have been distilled into a comprehensive chart created by Isuru Seneviratne, who monitors state electricity data for the advocacy group Nuclear NY.)

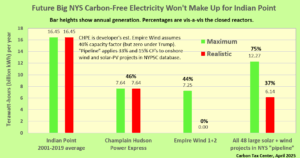

Renewables won’t soon make up Indian Point’s lost output

Renewable-power sources being developed for NY State can be placed in three groups.

- 1,200 megawatts (MW) of new hydroelectric power being brought to NY State from Quebec via a new 339-mile long transmission line known as the Champlain Hudson Power Express (CHPE).

- Wind farms in the Atlantic Ocean off Long Island, beginning with the 2,070-MW Empire Wind 1 and 2 arrays south of Long Beach (my hometown).

- New utility-scale on-shore wind and solar in various stages of permitting and construction, comprising nearly 50 ventures totaling around 7,000 MW.

Empire Wind generation is zeroed out in “realistic” scenario due to Trump’s fear and loathing of offshore wind. Realistic scenario for solar and (onshore) wind in project pipeline assumes one-half of maximum generation.

The raw megawatt figures above may appear imposing, but less so when we account for three crucial factors:

(i) Only CHPE can provide reasonably consistent electricity, with a capacity factor between 70% and 75%; the wind and solar farms are weather- and astronomically-limited to much lower annual outputs: I posit 40% (offshore wind), 33% (onshore wind) and 15% (solar).

(ii) Offshore wind is almost certainly dead in the water (sorry!), due to the U.S. president’s implacable hatred (rooted in his belief that a nearby wind-power venture would threaten the profitability of one of his Scotland golf courses). [See addendum at end of this post.]

(iii) Not all projects in the state renewables “pipeline” will prevail through permitting obstacles, local opposition and financing problems.

The bar chart at right adjusts for these factors by presenting the prospective the three categories of new carbon-free electricity alongside Indian Point in annual terawatt-hours. The green bars sum to 27 TWh, indicating total new carbon-free generation nearly two-thirds greater than that lost when the nuke plant was taken away. The more-realistic red bar sum, 13.8 TWh, is only around half of the maximum, and is less (by 14%) than Indian Point’s lost contribution.

Let’s also face that having new renewables make up for the generation lost by closing Indian Point is a pathetically low bar. New wind and solar were supposed to contribute mightily to stopping climate change by pushing fossil fuels out of the grid . . . which they cannot do at present if their output must stand in for the carbon-free output that Indian Point was prevented from providing after 2020.

Lessons learned?

The outlook for decarbonizing the NY State power grid is grim, even if there’s a post-Trump world in which the U.S. government doesn’t throttle offshore wind as it has tried (unsuccessfully, thank goodness) to scuttle New York’s congestion pricing program. As the last bar chart shows, even bringing Empire Wind to fruition won’t make up half of Indian Point’s lost carbon-free output.

And this post hasn’t touched on the closure’s prospective toll on downstate electricity rates and reliability. Nor has it treated the possibility that deteriorating U.S.-Canada relations will put a crimp in (or surcharges on) hydro-electricity from CHPE whose expected commencement next year is the only bright spot on the horizon, so far as large projects are concerned. (Rooftop solar has gained a solid foothold in New York State, which ranks third in the U.S. in the number of homes with solar panels, according to Solar Insure. Yet making up for Indian Point’s lost carbon-free output would require roughly one million new solar homes in the state — a 5-fold addition to the 200,000 existing solar homes in the state at the end of 2024.)

Here are three lessons learned from the premature closure of Indian Point:

Lesson #1. A robust carbon tax might have saved Indian Point. Based on its average 2001-2019 electricity output, a tax of $100 per ton of emitted CO2 would have conferred an annual carbon-avoidance value of three-quarters of a billion dollars on the Indian Point plant. (Calculation: 16.5 TWh/year x 10^9 kWh/TWh x 0.9 lb of CO2/kWh (per EIA, reduced slightly from that source’s 0.96 lb average to weed out peaker plants) x 1/2000 tons per lb x $100/ton.) A monetary bounty of that magnitude would have made it more difficult for Riverkeeper and then-Gov. Andrew Cuomo to engineer Indian Point’s closure. (During the decade preceding closure, the actual price under the Regional Greenhouse Gas Initiative (RGGI) to emit a ton of CO2 averaged 20 times less: around $5/ton.)

Image from my 2020 post bemoaning the pending closure of Indian Point. (Link in text at right. Gotham Gazette ceased publication in 2023.)

Lesson #2. Self-appointed environmental-interest groups should not be the primary arbiter of the public interest in climate-critical matters. “Climate was not at the table when Indian Point’s fate was being sealed,” I wrote in May 2020, weeks after Indian Point began to be shut down. Riverkeeper was at the table, of course, supported by several other prominent environmental organizations whose institutional biases led them, in my view, to overestimate the real-world availability of wind and solar electricity, undervalue Indian Point’s carbon-free benefit, and over-emphasize the risks of the nuclear plant’s continued operation. The result was that the “climate consequences of shutting Indian Point [were] brushed aside,” as suggested in the subhead to my 2020 post.

Lesson #3: New Yorkers must consider adding more nuclear power capacity to the state grid. I’m starting to re-evaluate the proposition that New York State can achieve a zero-emissions electric grid without adding considerable nuclear power capacity. This widely held viewpoint (“article of faith” might be a more apt term) was critiqued in late 2023 by PhD physicist and policy analyst Leonard Rodberg, whose analytical acumen and probity I’ve admired since the 1970s, when we were colleagues in the safe energy movement, as it was then called. Len’s detailed analysis concluded that approximately 29 GW of new nuclear capacity — the equivalent of 15 Indian Point plants — will be required in addition to large amounts of offshore wind as well as solar and other “distributed” power — to reliably and affordably decarbonize the state grid by 2040 while satisfying load growth from electrifying much of the space heating and vehicular transportation now provided by combusting fossil fuels.

Addendum

Heatmap and other news outlets reported on May 20 that the U.S. Interior Department lifted its April 16 stop-work order indefinitely halting construction of the 810-MW Empire Wind 1 in the Atlantic Ocean south of Nassau County, NY. This hopeful development is tempered, however, not just by the Trump administration’s notorious fickleness but by the fact that if and when completed the 810-MW wind farm will offset only a sixth of the carbon benefit that was destroyed by Gov. Andrew Cuomo and Riverkeeper’s closure of Indian Point. See graph.

{kind=link}